Diving into FrxEth

Diving into FrxEth

A new LSD to butt heads with Lido and Rocketpool. A new bull run for Eth?

An Overview

FraxEth is a new component of the Frax family of protocols. It is a staking service just like Lido or Rocketpool with major design differences.

Frax Finance began as a fractional stablecoin protocol, with FRAX being the flagship stablecoin product. The stablecoin design uses FXS (“Frax Shares”) as the endogenous collateral, allowing folks to mint FRAX by combing a 1 dollar amount of USDC and FXS.

The FraxEth ecosystem has no connection to FRAX aside from the fact that both ecosystems share FXS as their governance token.

The FraxEth ecosystem has two new tokens of interest: FrxEth (“frax Eth”), and sFrxEth (“staked Frax Eth”).

The FraxEth ecosystem poses a major challenge to incumbent players such as Lido and Rocketpool, and can translate into major price action in FXS.

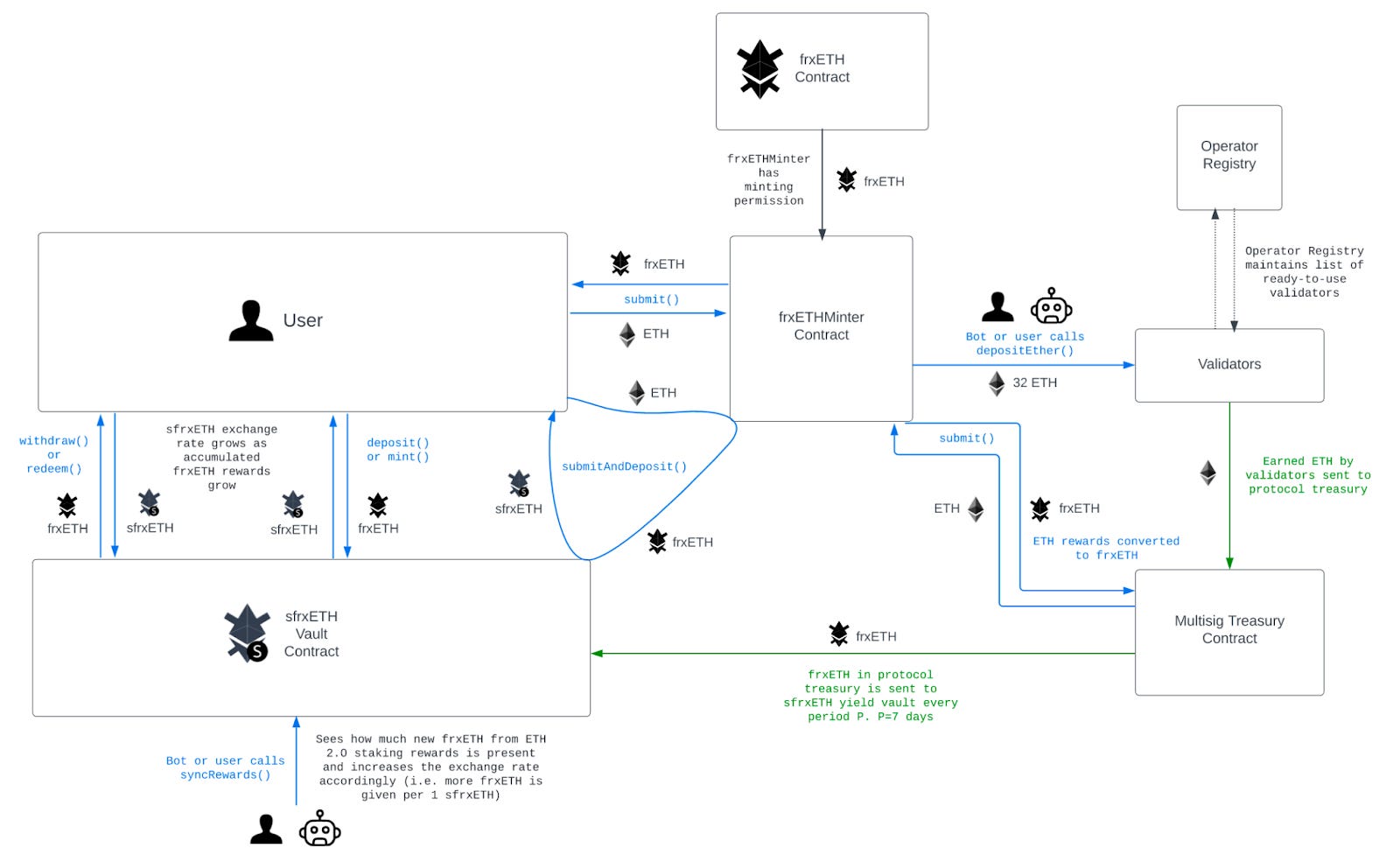

FrxEth & sFrxEth

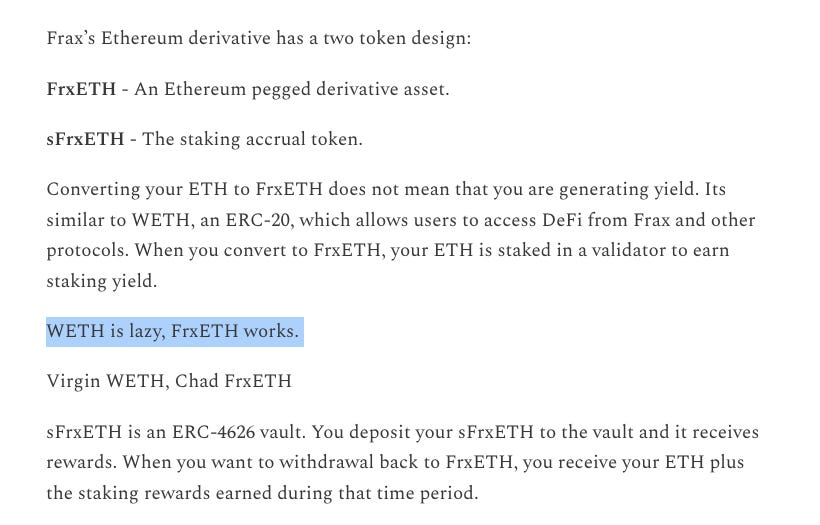

FrxEth (“Frax Eth”), an Erc20, is the liquid staking token invented by Frax Finance. FrxEth can be viewed as a stablecoin of Eth. FrxEth is minted when you stake Eth (and only Eth, no involvement of FXS here) at the FrxEth module. FrxEth cannot be redeemed back into Eth until after the Shanghai upgrade (early 2023) - same with Steth.

Under the hood, FrxEth is already Eth staked, which is why redemption is not possible until after Shanghai. Holding FrxEth does not entitle one to the yield from staking rewards.

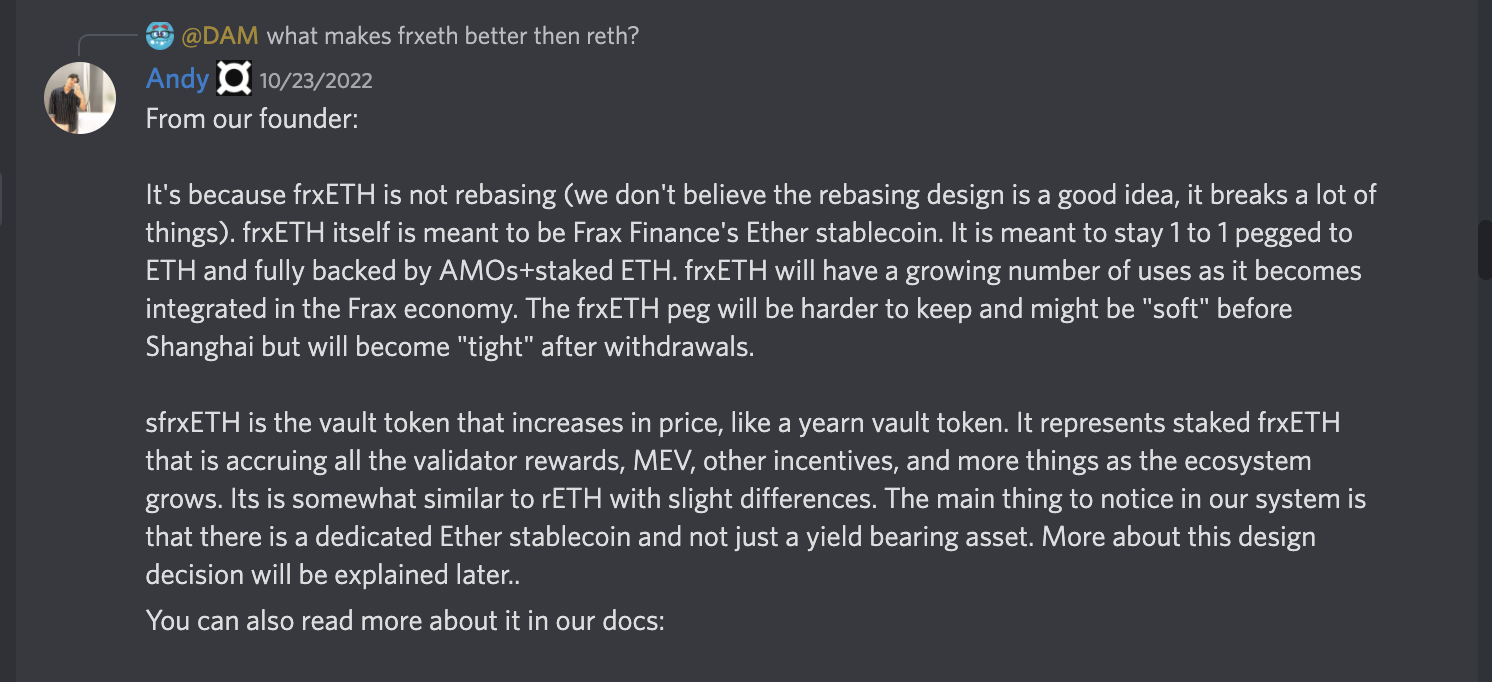

FrxEth does not rebase. It trades 1-1 to ETH. FrxEth is 100% backed by Eth. It is NOT a fractionalised eth-stablecoin. Fxs, which plays the role of expanding Frax supply by providing endogenous capital, plays no role in FrxEth except for the role of governance. A FrxEth-Eth depeg is therefore only going to happen in transitory periods where FrxEth-Eth liquidity is a problem.

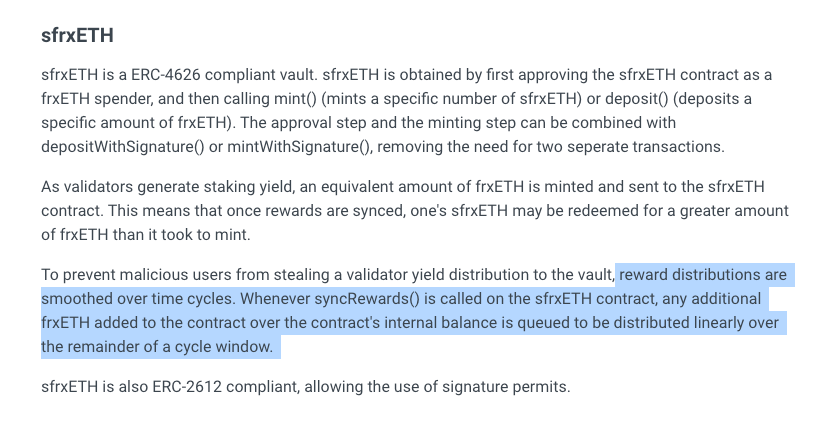

To obtain those rewards from the Eth staked, one must stake the FrxEth, and obtain sFrxEth. sFrxEth does not rebase. One can withdraw from staking and obtain FrxEth at any time, along with staking rewards in FrxEth (not Eth!). Its price should therefore be ever-increasing at the rate of yield. sFrxEth is an ERC4626 token - it is an extension of the ERC20 standard.

Why is FrxETH necessary?

Some folks find it difficult to understand why FrxEth is architecturally necessary. I have read through the docs and here’s my attempt to reverse-engineer the architectural design logic

Suppose you’re building a liquid staked Eth solution, suppose we call it sEth.

The typical and straightforward design logic would work like this. You’d envision sEth to be an ERC4626 token - essentially a receipt of a deposit into a vault. Deposit Eth into the vault, and then the vault mints you a sEth. The Eth deposited is then sent to a validator to accumulate validator yields, and when one withdraws, the principal along with the yield is distributed back to the holder.

There are a couple of issues here, which ultimately motivate the token to be rebasing. Since the Eth deposited to the validator and the yield accumulated would not be redeemable until the Shanghai upgrade, the Eth represented by 1 sEth would gradually increase as yield accumulates. This would mean the price of 1 sEth would gradually increase relative to 1 Eth. This is fine, of course, but you do want sEth be pegged to ETH so you’d get some nicer DeFi properties. Pegging it to Eth would give sEth some stablecoin premium in terms of adoption. If you are going to use it as collateral, sEth being pegged to Eth makes borrowing and lending - and therefore, looping - easy to manage. If sEth ain’t pegged to Eth, the price of sEth would be continuously increasing by the yield, then a staked-Eth shoved into a Compound as collateral would see continuously increased room for borrowing - such a design has baked-in capital inefficiency.

One solution to this is that you can adopt a rebasing design. You calculate the amount of Eth that has already been accumulated, and then you “send” an equivalent amount of sEth to the sEth holder. But “sending” tokens like this is highly impractical gas-wise. So you code your sEth such that the account balances of a holder automatically change. This is called rebasing.

But the issue here is that rebasing is very clumsy. To compete with Lido StEth and Rocketpool Eth, you will naturally want your liquid staked Eth to be usable in as many DeFi protocols as possible. So you don’t want sEth to be rebasing, because rebasing tokens are notorious to work with on a code level. Instead of just plugging you into the existing infrastructure, DeFi protocols and CEXes will have to design specific integration infrastructure to onboard you, the trouble might be such that they might not bother at all. So, no rebasing it is then.

To resolve this “to peg or not to peg” problem, Frax’s solution is to split the sEth token into two: FrxEth and sFrxEth.

FrxETH is Eth already staked, but you give up the yield. You get the yield only if you stake your FrxETh, which gives you the sFrxETh. Both frxETh and sFrxETh are fungible, so you get DeFi composability.

FraxEth as a competitor to WEth

There’s still the legitimate question as to who the hell would want to hold FrxETH? Why would you want to hold a kind of Eth that you cannot pay gas with at the cost of giving up yield? It’d seem like FrxEth holders are wankers.

As far as I can tell, this is not something they have in the roadmap but I wouldn’t be surprised if the Frax community eventually pushes to aggressively replace WEth with frxEth wherever they can - particularly in NFT Finance protocols. FrxEth is basically just WEth, but with the option to be staked and earn yield. WEth is strictly dominated by frxEth in terms of utility. It would also make sense that DAOs would prefer frxEth to WEth - stake it into sFrxEth while it is idle.

The Curve-Convex-Frax ecosystem - Deep Liquidity

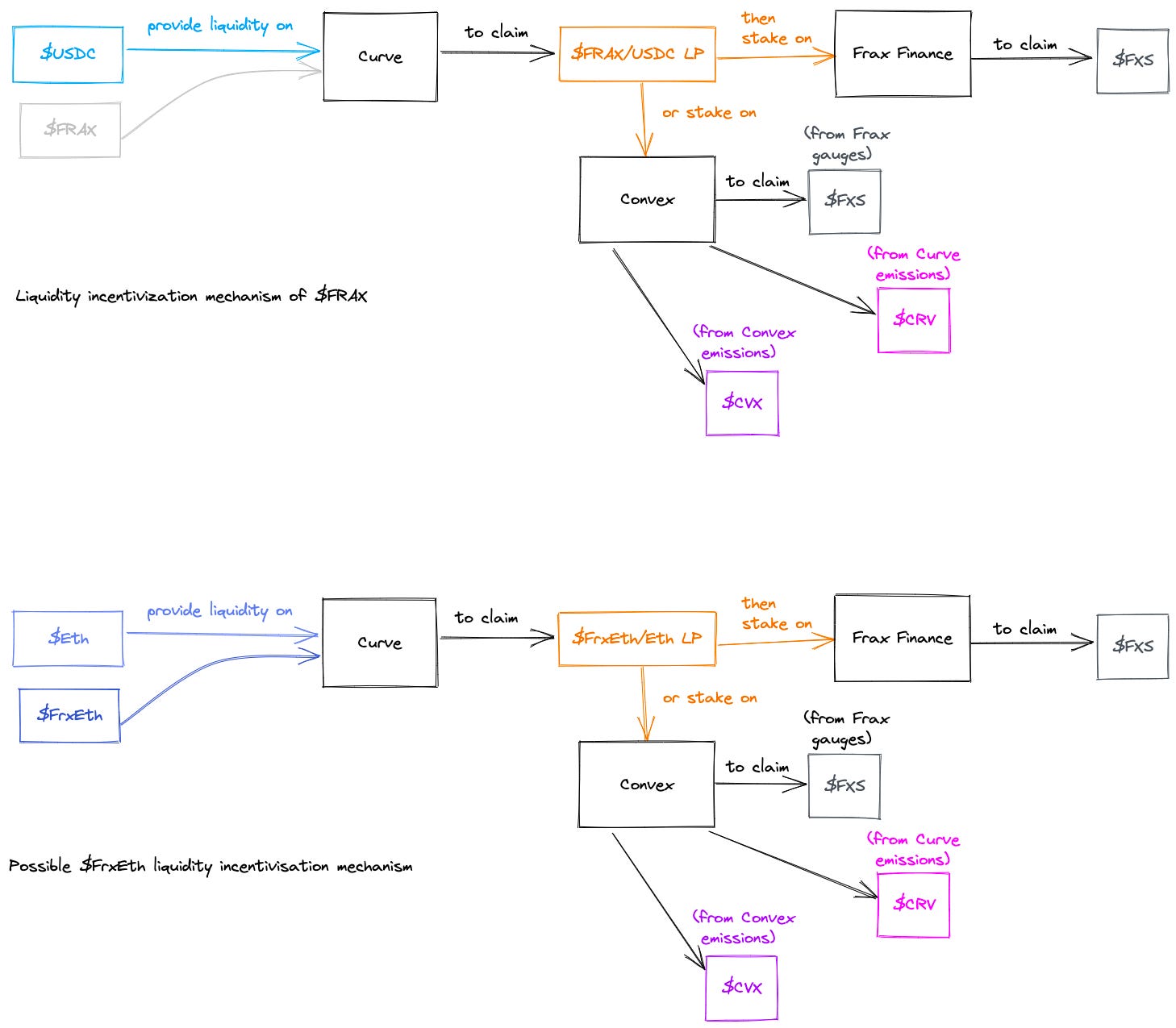

Deep liquidity matters because it inspires confidence, therefore adoption, therefore trading, therefore fees. Thin liquidity is deathly for stablecoins. Frax Finance has a couple of tricks up their sleeves to ensure thick liquidity for FrxEth and sFrxEth: through (1) their own staking contract and their AMOs, (2) the Curve-Convex ecosystem, (3) the Frax Basepool on Curve.

The Convex-Curve ecosystem has always played an integral part in ensuring deep liquidity for the Frax Ecosystem. One of the ways Frax consolidates its liquidity for USDC-FRAX pairs is through Convex. Note that Frax is the largest holder of CVX.

Liquidity is incentivized thus: you provide liquidity with USDC and FRAX on Curve, which mints you an LP token. If you don’t want to stake that LP token into Frax Finance because you find their yields to be unsatisfactory, you can take that to Convex which gives you a higher yield, which comes from a combination of FXS, CRV, and CVX emissions. Frax merely needs to replicate this structure with FrxEth and sFrxEth and viola.

This integration with Curve and Convex is integral to frxEth’s success, as frxEth’s bets on its advantage being that sFrxEth will be able to generate a higher yield than stEth because some frxEth will be giving up the yield - but for CRV, CVX, and FXS.

There is a legitimate question though on whether emissions will be great enough for FrxEth liquidity providers to forgo the sFrxEth yield - or rather, perhaps the more apt comparison is whether such emissions are going to be greater than the yield obtained by simply holding stEth. We shall cover this below.

A frxEth Base Pool? frxEth AMOs?

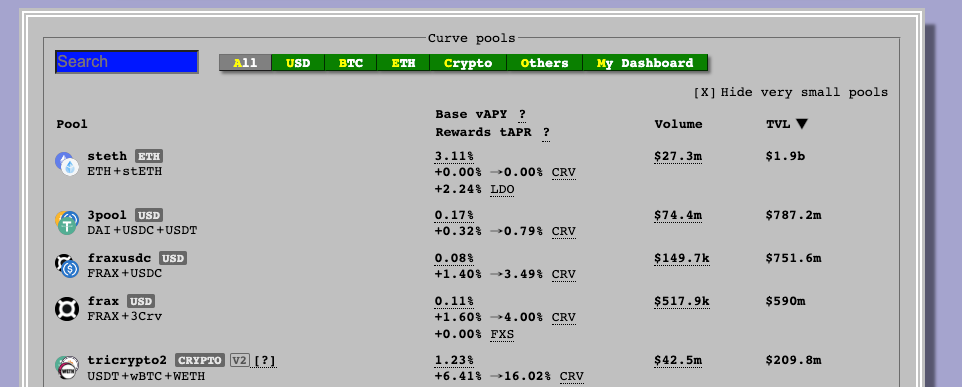

On May 26, 2022 (two weeks after Luna), Frax submitted a proposal on the Curve governance form on deploying a FraxBP pool. This allows the construction of metapools.

A base pool is a pool whose LP tokens are used to pair with another token. A metapool pairs a coin against the LP token of another pool. This other pool is referred to as the “base pool”. By using LP tokens, metapools allow swaps against any asset within their base pool, without diluting the base pool’s liquidity.

Curve’s factory contract only allows the deployment of metapools using a handful of base pools, namely the 3pool (for USD denominated assets) and the sBTC (for BTC denominated assets) base pools, until Frax submitted the aforementioned governance change which created the FraxBP.

The significance of a Frax base pool is that stablecoins face a choice to pair with the FraxBP or the 3CRV pool. As long as rewards are higher than 3CRV, stables will choose FraxBP, and there is a good reason why FraxBP (the fraxUSDC pool) has and will likely continue to have a higher APY than the 3pool. This is thanks to the Curve AMO built by the gigachads at Frax. An AMO (“Algorithmic Market Operations Controller”) is an autonomous contract that enacts arbitrary monetary policy so long as it does not change the FRAX price off its peg. To put it short, an AMO looks at the collateral ratio right now, and calculates the amount of USDC needed to honour redemptions at that collateral ratio. Any USDC excess to that amount is effectively idle, and so an AMO takes that USDC, pairs it with FXS to mint FRAX without going below the collateral ratio, and then shove the FRAX to somewhere it could earn yield. In particular, the Curve AMO puts FRAX and USDC collateral to work providing liquidity for the protocol and tightening the peg. This means part of the liquidity for FRAX is protocol-owned, and the CRV earned therein is then used to vote for more emissions. (more on this below)*

Is there’s going to be a frxEth base pool? If yes, how will it sustain its own liquidity? Indeed, how is it supposed to dethrone Lido’s Eth-stEth pool’s 1.9b liquidity. For perspective, Lido spends 48M $LDO (~$72m) per year to sustain that. LDO treasury has ~$260m.

Here we are wading into speculative territory, and my guess is that without an AMO, liquidity on a frxEth BP would be difficult to incentivize as you would have to direct some of the crv voting power from elsewhere (like the FraxBP) to incentivize the frxEth BP.

But how is a frxEth AMO going to work? Unlike Frax, frxEth is not a fractionable stablecoin. There is no “idle” equivalent of the USDC to be paired with FXS to mint FRAX to be sent elsewhere for yield.

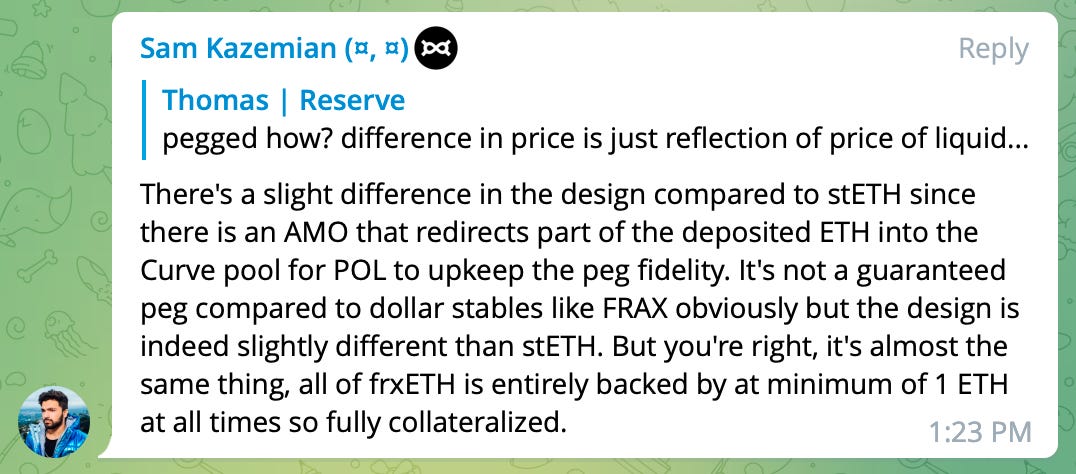

from the flywheeloutput substack: everything we know about frxEth so far

If I have to guess, I’d guess a frxEth AMO would work like this. As long as there is a difference in the time in which new frxEth yield is generated and the time in which frxEth balance is accredited to a user’s balance and made withdrawable, the frxEth that is generated through yield but not accredited can be considered idle, and therefore sent to do work.

To follow the documentation parlance, whenever frxEth in the sFrxEth contract is not synced via the syncRewards() function, it could be taken to do something else. This is my two cents on a possible frxEth AMO design.

Validator situation

As of this moment, all Frax validators are in-house, and there is no documentation on how to participate.

Aside from questions on when validator applications will be open, there are questions on whether the relayer will be censorous. My guess is that FXS will be used for the voting of the onboard of validators and that the infrastructure will take a non-ideological design with regards to OFAC censors - whatever makes more money.

Aside from all that we do not know much besides. Lido deducts a portion of staking yield (typically 10%) as a fee before passing the rest on to stEth holders, and the fee deduct is split 50-50 between the validators and the LIDO treasury.

For frxEth, according to a governance proposal, the protocol fee structure for frxEth will initially involve:

A minimum of 90% of ETH earned rewarded to sfrxETH vault stakers in the form of frxETH;

8% of earned ETH to Frax Protocol treasury in the form of frxETH. This ultimately will be distributed back to FXS holders;

A slashing Insurance Fund: 2% goes into a fund to cover potential slashing events/unforeseen penalties to cover frxETH deposits to effectively keep frxETH overcollateralized at over 100% CR to cover any possible issues/losses;

This structure will have to be modified once frxETH can support independently run validators in v2. There will have to be a validator-protocol split added to the structure. The current structure assumes that the Frax Protocol is the only entity running validators and thus the 8% fee covers the “validator fee” portion. This will not always be the case.

Naturally, this 8% fee distribution to FXS is bullish for FXS.

But the issue here is that there is right no documentation nor tokenomics to incentivise the scaling of the army of validators. Will FXS be used as collateral to cover for penalties or slashing losses like in Rocketpool? We still don’t know. We also don’t know how MEV will play in this part of Frax’s architecture.

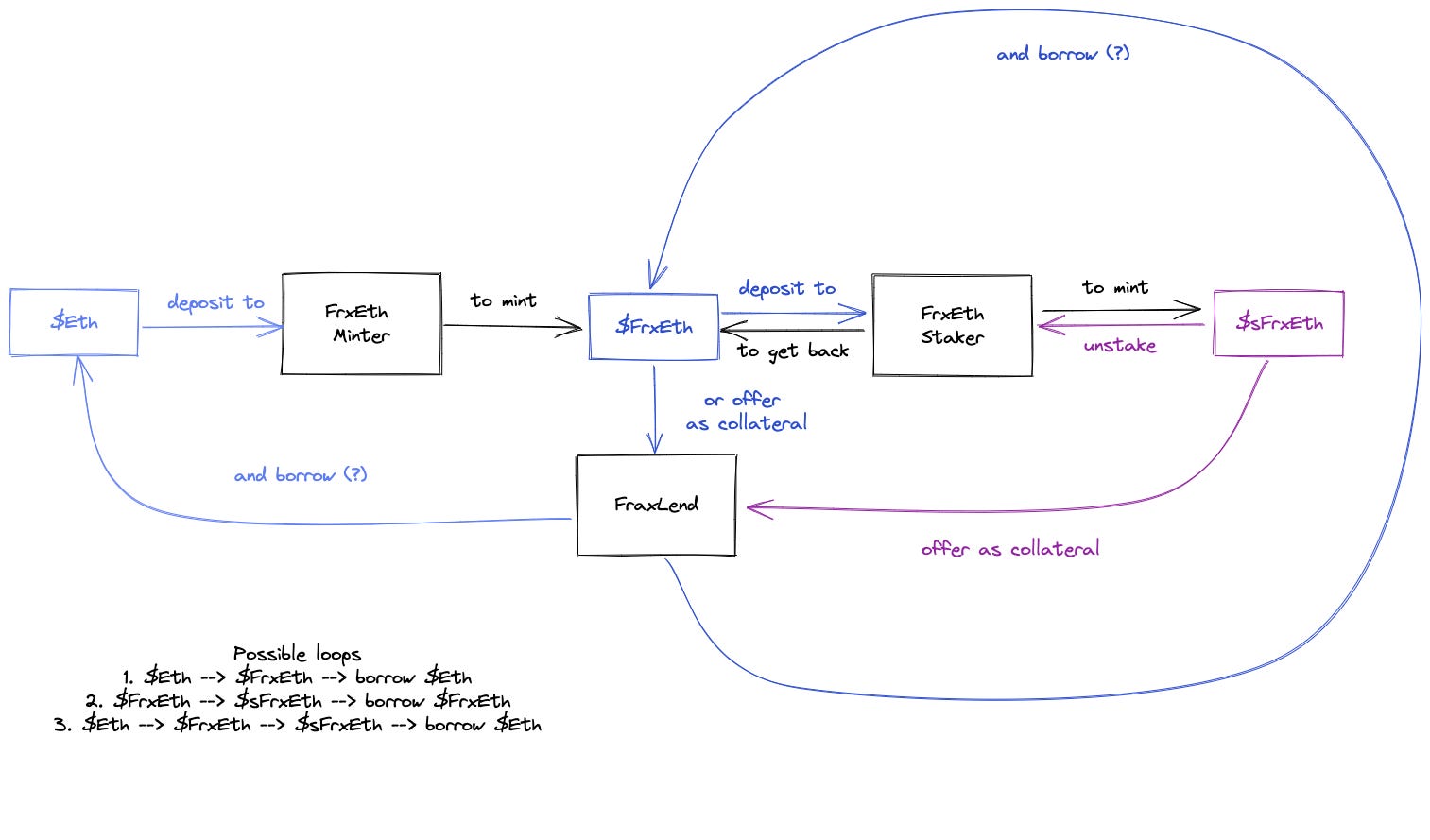

Looping strategy - a new Eth bull run?

Anyone who’s been alive in 2022 can smell FraxEth’s architecture begging for a looping strategy, and instead of letting Euler get all the fun, obviously Frax will leverage their very own Fraxlend to maximise usage of their own protocol - Sam Kazemian has confirmed this.

Assuming Eth, frxEth, and sFrxEth are all made borrowable and lendable on Fraxlend, there could be 3 possible strategies:

Stake Eth to mint frxEth → deposit frxEth to FraxLend → borrow Eth to mint frxEth.

Stake frxEth to mint sFrxEth → deposit sFrxEth to FraxLend → borrow frxEth to mint sFrxEth.

Stake Eth to mint frxEth → Stake frxEth to mint sFrxEth → deposit sFrxEth to FraxLend → borrow Eth to mint frxEth.

Out of these three strategies, (2) has arguably the lowest risk, and is most not subject to the kind of “depeg” liquidation we’ve seen with Eth-stEth looping strategies. If liquidity on Curve fails, (1) and (3) would both be rekt as it is not possible to unstake frxEth to redeem Eth until the Shanghai upgrade.

The possibility of such looping strategies have generated discussion as to whether FraxEth will be so sexy such that people will start mass locking Eth, galvanising a new bullrun. On the other hand it also has one wonder if we will see another 3AC or Celsius implosion situation thanks to looping and liquidations.

P.S. AMOs - my understanding

Minting and redeeming FRAX is governed by the following set of equations

Suppose Alice minted 1 FRAX at a collateral ratio of 1. Then Frax the protocol would have 1 USDC, and 0 FXS shares. Suppose then the protocol decreased the collateral ratio down to 0.8. Then to mint 1 FRAX, then you just need 0.8 USDC and 0.2 FXS. So then Frax the protocol would have 1.8 USDC and 0.2 FXS in total, assuming (for the sake simplicity, that the price of FXS is 1$). The collateral ratio of the protocol is then 0.9 (just plug in the figures into the second equation), which is higher than 0.8. To put it another way, you now have 2 FRAX, and to redeem them both at a collateral ratio of 0.8 you just need 1.6 USDC and 0.4 FXS. So you have 1.8-1.6 = 0.2 USDC sitting here idle doing nothing. The point of an AMO is then to mint FRAX by pairing that USDC with FXS and earn yield on it.

Thanks for reading Reflexivity Engine! Subscribe for free to receive new posts and support my work.

Great write-up. Thank you.